09 Apr April 2023 Update

How Does Tax Apply to Electric Cars?

Just in time for the Fringe Benefits Tax (FBT) year that started on 1 April, the Australian Taxation Office (ATO) has released new details on electric vehicles.

The FBT exemption for electric cars

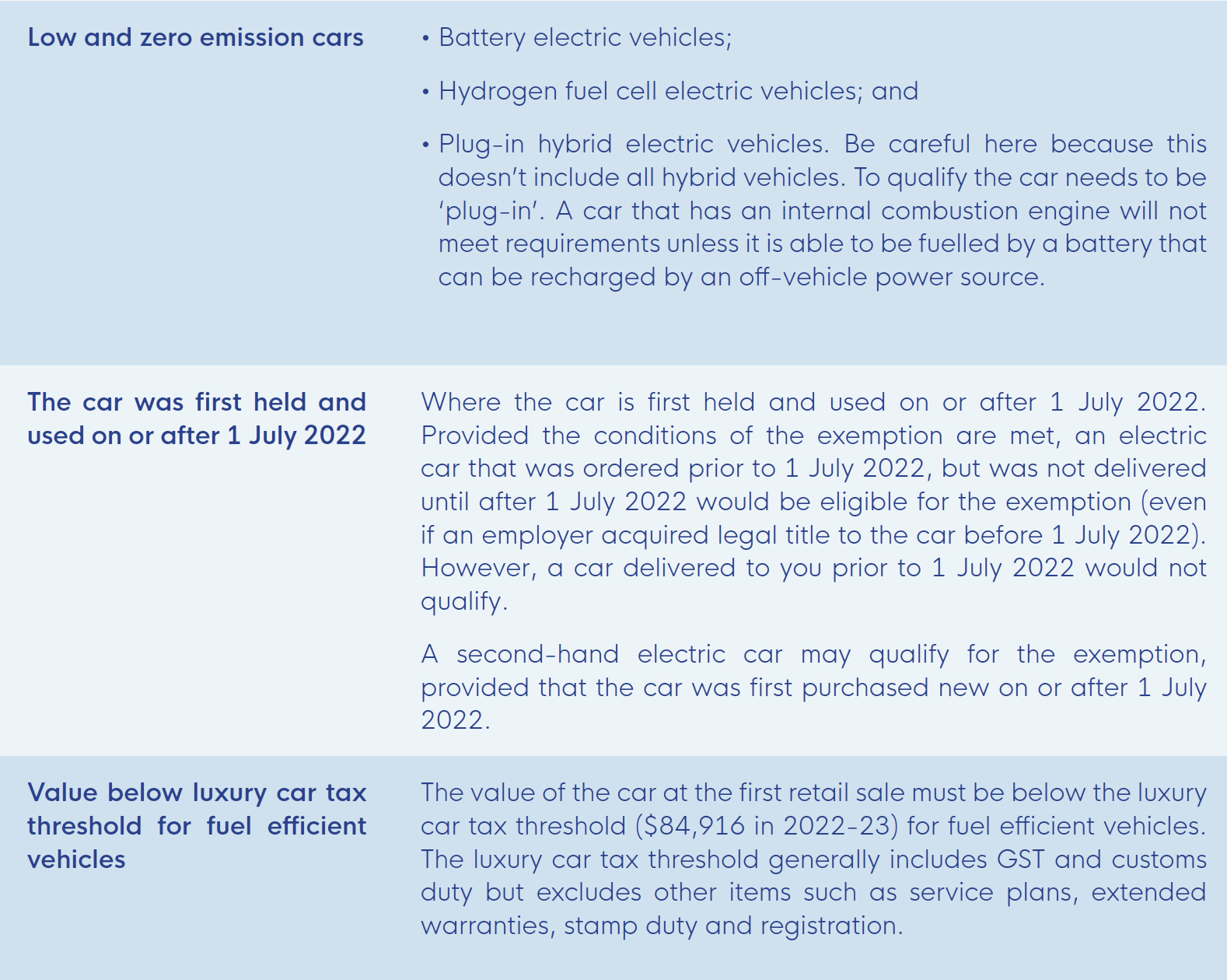

If your employer provides you with the use of a car that is classified as a zero or low emissions vehicle there is an FBT exemption that can potentially apply to the employer from 1 July 2022, regardless of whether the benefit is provided in connection with a salary sacrifice arrangement or not. The FBT exemption should normally apply where:

- The value of the car is below the luxury car tax threshold for fuel efficient vehicles ($84,916 for 2022-23) when it was first purchased. If you buy an EV second-hand, the FBT exemption will not apply if the original sales price was above the relevant luxury car tax limit; and

- The car is both first held and used on or after 1 July 2022. This means that the car could have been purchased before 1 July 2022, but might still qualify for the FBT exemption if it wasn’t made available to employees until 1 July 2022 or later.

The exemption also includes associated benefits such as:

- Registration

- Insurance

- Repairs or maintenance, and

- Fuel, including electricity to charge and run the vehicle.

But, it does not include a charging station (see How do the tax rules apply to home charging units?).

While the FBT exemption on EVs applies to employers, the value of the fringe benefit is still taken into account when working out the reportable fringe benefits of the employee. That is, the value of the benefit is reported on the employee’s income statement. While you don’t pay income tax on reportable fringe benefits, it is used to determine your adjusted taxable income for a range of areas such as the Medicare levy surcharge, private health insurance rebate, employee share scheme reduction, and certain social security payments.

Who the FBT exemption does not apply to

By its nature, the FBT exemption only applies where an employer provides a car to an employee. Partners of a partnership and sole traders are not employees and cannot access the exemption personally.

If you are a beneficiary of a trust or shareholder of a company, the exemption can only apply if the benefit is provided in your capacity as an employee or as a director of the entity (you need to be able to show you have an active role in the running of the entity).

How do the tax rules apply to home charging units?

The ATO has confirmed that charging stations don’t fall within the scope of the FBT exemption for electric cars. This means that FBT could be triggered if an employer provides a charging unit to an employee.

If an employee purchases a home charging unit then it might be possible to claim depreciation deductions for the cost of the unit over a number of income years if the unit is used to charge a vehicle that is used for income producing purposes. However, if an employee is only using the vehicle for private purposes then the cost of the charging unit is a private expense and not deductible.

What about the cost of electricity?

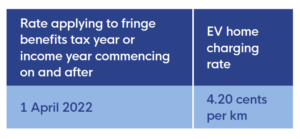

A friend of mine travels a lot for work and used to rack up large travel expenses…right up until he switched to an electric vehicle. Now it costs him 3 cents per km in electricity.

Because it is often difficult to distinguish home electricity usage, the ATO has set down a rate of 4.20 cents per km for running costs for EVs provided to an employee (from 1 April 2022 for FBT and 1 July 2022 for income tax).

If you use this rate, you cannot also claim any of the costs associated with costs incurred at commercial charging stations. It is one or the other, not both.

You also have the option of using actual electricity costs if you can calculate them accurately.

Selling a business? The pros and cons of earn-out clauses

Earn-out clauses for the sale of a business are increasingly common. We look at the positives and negatives that every business owner should consider.

Business transactions often include earn-out clauses where the vendors ‘earn’ part of the purchase price based on the performance of the business post the transaction. Typically, an earn-out will run for a period of one to three years post transaction date.

There are two main reasons to include an earn-out in a sale:

- To bridge a gap in the sale price expectations between the vendor and the purchaser. The earn out represents an ‘at risk’ form of consideration. If the business produces the result, the vendors are rewarded through a higher sale price.

- To incentivise the vendors who are continuing to work in the business and maintain the growth momentum of the business post sale.

Advantages of earn-outs include:

- The ultimate sale price has a performance component to it – both buyer and seller benefit.

- May assist in achieving a sale where a price impasse would otherwise prevent the sale.

- If the calculation of the earn-out is transparent and easily measurable, there should be no dispute between the parties.

- Creates equity where the business has lagging income, new business initiatives in play at the time of sale or a high growth rate.

- The incremental sale price can be effectively funded by the business out of realised growth.

The key to an effective earn-out is in their construction, both from a commercial and a legal perspective. Get them right and they can enhance the continuity and succession of a business.

Company money: A guide for owners for owners

When you start up a business, inevitably, it consumes not just a lot of time but a lot of cash and much of this is money you have already paid tax on. So, it only seems fair that when the business is up and running the business can pay you back. Right?

There a myriad of ways owners look for payback from a company they have invested their time and money into it from dividends, salary and wages, jobs for sometimes underqualified family members to cash advances and personal expenses like school fees and nights out picked up as a company expense. But, once the cash is in the company, it is company money.

We look at the flow of money in and out of a company and the problems that trip business owners up.

Repaying money loaned to the company

If you have lent money to your company, you can draw this money back out as a loan repayment. The loan repayment is not deductible to the company but any interest payments made to you will be as long as the borrowed money has been used in the company’s business activities (assuming interest has actually been charged on the loan).

Conversely, any repayments made by the company on the loan principal are not income for tax purposes but you will need to declare any interest earned in your income tax return. All loans, including the loan term and repayments, should be documented.

Dividends: Paying out profits

Dividends basically represent company profits being paid out to the shareholders of a company. If the company has franking credits from income tax it has paid, the dividends might be franked and the credits can often be used by the shareholder to reduce their personal tax liability.

When a dividend is paid by a private company it must provide a distribution statement to the shareholders within four months after the end of the financial year. This gives private companies up to four months after the end of the financial year to work out the extent to which dividends will be franked.

If any of the shares in the company are held by a discretionary trust then there are some additional issues that will need to be considered, including whether the trust has a positive amount of net income for the year, whether the trust has made a family trust election for tax purposes and who will become entitled to distributions made by the trust for that year.

Repaying share capital

Many private companies are set up with a relatively small amount of share capital. However, if a company has a larger share capital balance then there might be scope for the company to undertake a return of share capital to the shareholders. Whether this is possible will depend on the terms of the company constitution and there are some corporate law issues that need to be addressed.

From a tax perspective, a return of share capital will normally reduce the cost base of the shares for CGT purposes, which means that a larger capital gain could arise on future sale of the shares but there won’t necessarily be an immediate tax liability. Having said that, there are some integrity rules in the tax system that need to be considered. The risk of these rules being triggered tends to be higher if the company has retained profits that could be paid out as dividends.

Shareholder loans, payments and forgiven debts: Using company money

There are some rules in the tax law (known as Division 7A) that determine how money taken out of a company is treated. Division 7A is a particularly tricky piece of tax law designed to prevent business owners accessing funds in a way that circumvents income tax. While amounts taken from a company bank account by the owners are often debited to a shareholder’s loan account in the financial statements, Division 7A ensures that any payments, loans, or forgiven debts are treated as if they were dividends for tax purposes unless there is a loan agreement in place which meets certain strict requirements. These ‘deemed’ dividends cannot normally be franked.

If you have taken money out of the company bank account then the main ways of avoiding this deemed dividend from being triggered are to ensure that the loan is fully repaid or placed under a complying loan agreement before the earlier of the due date and actual lodgement date of the company’s tax return for that year. To be a complying loan agreement the agreement requires minimum annual repayments to be made over a set period of time and there is a minimum benchmark interest rate that applies – currently 4.77% for 2022-23.

For example, if your company is paying school fees for your kids, or you take money out of the company bank account to pay down your personal home loan, if you don’t pay back this amount or put a complying loan agreement in place then this amount is likely to be treated as a deemed unfranked dividend. That is, you need to declare this amount in your personal income tax return as if it was a dividend and without the benefit of any franking credits. This means that even though the company might have already paid tax on this amount, you will be taxed on it again without the ability to claim a credit for the tax already paid by the company (causing double taxation of the same company profits).

The rules are very strict when it comes to loan repayments. If a repayment is made but the same amount or more is loaned to the shareholder shortly afterwards then there are some special rules that can apply to basically ignore the repayment. There are some exceptions to these rules and the position needs to be managed carefully to avoid adverse tax implications.

Update: Tax on super balances above $3m

In a very quick turnaround from announcement to draft legislation, Treasury has released the exposure draft legislation for consultation to enact the Government’s intention to impose a 30% tax on future superannuation fund earnings where the member’s total superannuation balance is above $3m.

The draft legislation confirms the Government’s intention to:

- Impose the tax on member accounts with superannuation balances above $3 million from 1 July 2025 (not indexed); and

- Apply the additional 15% tax to ‘unrealised gains’. This will mean that a tax liability will arise if the value of the assets goes up

Currently, all fund income is taxed at either 15%, or 10% for capital assets that have been held by the fund for more than 12 months. Unrealised gains, that is gains that are made because of changes in value, gains on paper, are not currently taxed – only when the gain is realised on sale or disposal of the asset.

If enacted, the legislation would mean that those impacted, could be paying tax on gains in value but without the cash from a sale to support the tax payment.

Budget 2023-24

The 2023-24 Federal Budget will be released on Tuesday, 9 May 2023. Look out for our update the next day on the important issues to you, your superannuation and your business.

Little has been released to date on the impending Budget beyond the tax on super balances above $3m and the decision not to extend the temporary $1,500 low and middle income tax offset beyond 30 June 2023.

Cost of living is a focus but on this, the Government is walking a tightrope between easing pressure without increasing inflation.

In the election cycle, if there is going to be a tightening, the mid-term Budgets are the time to do it. The Government will undoubtedly look at concessions provided within the tax system and whether those concessions meet their stated objective and when it comes to spending, potentially redraw the allocations. Some of the areas to watch include:

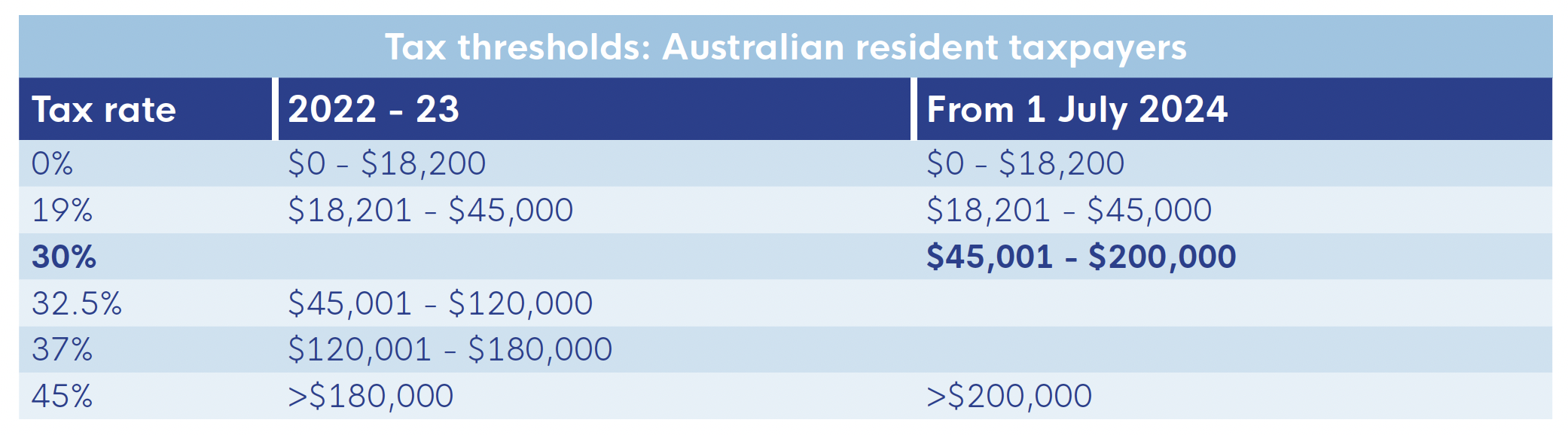

- The legislated stage three tax cuts, that collapse the 32.5% and 37% tax brackets to a single rate of 30% for those with assessable income between $45,000 and $200,000 are not due to commence until 1 July 2024. The Government committed to keeping the tax cuts during the election and can bypass the issue until the 2024-25 Budget, but we’ll see.

- Provision for announced defence spending.

Active support to develop a viable clean energy industry and transition to clean energy (see the joint submission from the Business Council of Australia, Australian Council of Trade Unions, World Wide Fund for Nature-Australia and the Australian Conservation Foundation).

- Productivity measures – Temporary full expensing – the productivity measure designed to encourage business investment that enables a business to fully expense the cost of depreciable assets in the first year of use – is set to expire on 30 June 2023. The Government will either extend, redevelop the small business instant asset write-off, or remove the concession altogether.

- Technology and training boosts – In the 2022-23 Federal Budget, the former Government announced that it would provide certain business taxpayers with ‘bonus’ tax deductions for investing in employee training or improving digital operations. The Skills and Training Boost allows small businesses (aggregated turnover less than $50 million) to claim a 120% deduction for eligible expenditure incurred on external training for employees between 29 March 2022 and 30 June 2024. The Technology Investment Boost provides a 120% deduction for eligible expenses that are incurred for the purposes of improving digital operations or digitising business operations. This can include the cost of depreciating assets. The boost is aimed at costs incurred between 29 March 2022 and 30 June 2023 and is limited to a maximum bonus deduction of $20,000. But, the legislation enabling both boosts has not passed Parliament. There is an opportunity in the Budget to extend the scope and nature of the concession.