16 Apr April 2024 Update

Warning on SMSF asset valuations

The ATO has issued a warning to trustees of SMSFs about sloppy valuation practices.

ATO data analysis has revealed that over 16,500 self managed superannuation funds (SMSFs) have reported assets as having the same value for three consecutive years. With many of these assets residential or commercial Australian property, you can forgive the ATO for being incredulous.

For trustees of SMSFs, where asset values are consistently reported at the same value, it’s likely your SMSF will be flagged for closer scrutiny by the ATO.

The value of assets in your SMSF impacts on member balances and by default, can impact the amount you can contribute, ability to segregate assets for exempt current pension income, the work test exemption and access to catch-up concessional contributions. And, as we move closer to the implementation of the Division 296 $3m superannuation tax, valuations will be very important for anyone with a member balance close to or in excess of $3m.

If the asset is an in-house asset, for example a related unit trust, then an accurate valuation is essential to ensure the fund remains within the 5% in-house asset limit. If the value of in-house assets rises above 5% of total assets, the asset/s need to be sold to bring the limit back below 5%.

Valuing at market value

Each year, the assets of your SMSF must be valued at ‘market value’ and evidence provided to your auditor. Broadly, market value is the amount that a willing buyer of the asset could reasonably be expected pay to acquire the asset from a willing seller assuming that the buyer and seller are dealing at arm’s length, and everyone acts knowledgeably and prudentially. It’s a common sense test that looks at the value you could reasonably expect to achieve for an asset.

If your SMSF holds collectible and personal use assets like artwork, jewellery, motor vehicles etc., a valuation must be performed by a qualified independent valuer on disposal. This does not necessarily mean that an independent valuation needs to be completed every year but at least every three years would be prudent. If you are not utilising an independent valuer, you will still need to make an active assessment based on market conditions. For example, if you hold artwork and the artist who created your investment artwork died, has this changed the value? Are the primary and secondary markets for the artwork transacting at a higher value? Leaving the value of the asset at its acquisition price calls into question the rationale for acquiring the asset within the fund in the first place. If the asset is unlikely to add any value to your retirement savings, then should it be held in your SMSF when you could achieve a higher rate of return elsewhere?

In most cases, the ATO require trustees to value an asset based on “objective and supportable data”. This means that you should document the asset being valued, a rational explanation for the valuation, and the method in which you arrived at it.

Valuing real property

Commercial and residential real estate does not need to be valued by an independent valuer. But, if there have been significant changes to the property, the market, or the property is unique or difficult to value, it is a good idea to have a written independent valuation from a valuer or estate agent undertaken (their report should also document the valuation method and list comparable properties).

If you are completing the valuation yourself, ensure that you document the time period the valuation applies to and the characteristics that contribute to the valuation. For example, a 10 year old brick four bedroom property on 640m2 of land in what suburb and any features that make it more or less attractive to a buyer, for example proximity to transport. And, you should access credible sales data either on similar properties in the same suburb that have sold recently or from a property data service. More than one source of data is recommended.

The estimates on a lot of online property sales sites are general in nature and not reliable for a valuation of a specific property. The average price change for the suburb however could be used as supporting evidence of your valuation.

For commercial property, net income yields are required to support the valuation. Where the tenants are related parties, for example your business leases a commercial property owned by your SMSF, you will need evidence that a comparative commercial rent is being paid and the rent is keeping pace with the market.

Valuing unlisted companies and unlisted trust investments

Valuing unlisted companies and unlisted investments can be difficult. The financials alone are not enough. But, if your SMSF invested in an unlisted company or shares in a unit trust, then there is an expectation that the trustees made the decision to make the initial acquisition based on the value of the asset, its potential for capital growth and income generation. That is, if you assessed the market value going into the investment, then it should not be a stretch to value the asset each year.

The difficulty for many investors is that in unlisted companies or trusts, the initial investment was broadly equivalent to the cash requirements of the activity being undertaken.

Generally, the starting point is the value of the assets in the entity and/or the consideration paid for the shares/units. For widely held shares or units, this is the entry and exit price.

Where property is the only asset, then the valuation principles for valuing real property are likely to apply.

Where there is no reliable data or market

We’ve seen a few scenarios where the assets purchased or created by the SMSF have no equal or there is no market – the true extent of the value will only really be known when the asset is realised. These unusual items default to either a professional valuation or a viable market assessment. This might be a derivative of the purchase price or data from a related market.

Valuations and the impending Division 296 tax on super earnings

The value of assets will be particularly important for those with super balances close to or above the $3m threshold for the impending Division 296 tax on fund earnings. Because the tax will measure asset values and tax the growth in earnings above the $3m threshold, accurate valuations will be important to ensure that the fund does not pay tax when it does not need to, and to reduce the likelihood of anomalies artificially inflating tax payable.

Budget 2024-25

The 2024-25 Federal Budget is the third for the Albanese Government and consistent with previous years, the primary themes are expected to be the cost of living and the economic shift to net zero. According to election guru Antony Green, the window for the next election starts on Saturday, 3 August 2024, “the first possible date for an election if writs are issued on 1 July. The election window will stay open until mid-May 2025, the last date being 17 or 24 May.” No doubt, the Government will have the election in mind when it presents the Budget on 14 May at 7.30pm AEST.

Stage 3 tax cuts

The redesigned stage 3 tax cuts have been passed by Parliament and will apply from 1 July 2024. The amendments broadened the benefits of the tax cut by focussing on individuals with taxable income below $150,000.

Investment incentives for small business

It remains to be seen whether an increased instant asset write-off threshold will apply to smaller businesses in the 2024-25 income year. The increased threshold to $20,000 announced in the 2023-24 Budget still has not passed Parliament (the Senate increased the threshold to $30,000). If the intent of this measure is to encourage investment, it is essential that legislation enabling these measures is passed by Parliament in a reasonable time to give business operators the certainty they need to commit to any additional investment spending.

Energy bill relief

The Prime Minister has hinted at another round of energy bill relief to ease cost of living pressures for low-income households and small business. The measure is subject to support from State and Territory governments.

The assault on professional services

The ATO has signalled that it is willing to pursue professional services firms who divert profits to avoid tax.

Two new cases before the Administrative Appeals Tribunal demonstrate how serious the Australian Taxation Office (ATO) is about making sure professional services firms – lawyers, accountants, architects, medical practices, engineers, architects etc., – are appropriately taxed.

In both cases, the ATO pursued the practices using Part IVA. Part IVA is an area of the income tax law that enables the Tax Commissioner to attack schemes or arrangements undertaken to obtain a tax benefit, enabling him to cancel any benefit derived by the scheme. That is, you could have a legally viable structure in place but if the only purpose of that structure is to reduce tax, then the Commissioner can use Part IVA to remove the tax

benefit. And, if Part IVA applies, you may end up with an additional tax liability as well as an administrative penalty of either 25% or 50% of the tax shortfall amount.

Broadly, the cases involved a solicitor who controlled a number of practice trusts that derived profits through marketing and facilitating tax planning arrangements.

While the arrangement in each case was complex and involved a large number of steps, the practice trusts ensured their business profits weren’t subject to tax by essentially making trust distributions on paper through a series of trusts and ultimately to either a company that had existing tax losses, or a tax-exempt entity. However, the real funds relating to the trust distribution (less a commission paid for the use of these entities) were ultimately received by the solicitor or their associated entities in the form of a loan.

Professional practices have been in the ATO spotlight for many years now for the way they distribute profits. Back in 2021, the ATO finalised its guidance on the allocation of professional firm profits, putting in place a series of risk ratings and gateway tests. These two cases however demonstrate the ATO’s willingness to pursue the issue in the courts using the Commissioner’s powers in Part IVA.

For professional services firms, it’s important to be aware that there are several ways in which the ATO can potentially challenge arrangements involving the distribution of profits from a professional practice. For example:

- If a trading entity derives personal services income that mainly relates to the skills and efforts of a particular individual, the ATO has certain expectations around ensuring the profits are assessed to the individual performing the work.

- If a trading entity doesn’t derive personal services income but income from a business structure involving a professional practice, the ATO has set out its compliance approach to targeting arrangements that don’t result in a reasonable level of profit being taxed in the hands of the individual practitioners.

- If a trust makes paper distributions to loss entities to ‘soak up’ deductions or losses, there are integrity rules in section 100A, another area of tax law under intense scrutiny, that need to be considered.

How much is my business worth?

For many small business owners, their business is their largest asset and for many, one that is expected to help fund their retirement. But what is your business really worth and what sets a high value business apart?

Every business owner is naturally curious about just how much their business is worth. However, for every business that sells at an attractive price, there are others that struggle to sell, let alone fetch a premium. The question is, what makes a difference?

When you come to sell a business the first question is, what are you selling? In most cases, this is fixtures and fittings, plant and equipment, stock on hand, and the goodwill of the business. Generally, a buyer won’t want to purchase your liabilities or your business structure, nor will they want to collect your outstanding debtors. Most business sales become a sale of business assets.

These assets are relatively easy to value with the exception of the goodwill. The value of plant and equipment and trading stock can generally be agreed. The tension tends to be around the value of the goodwill because goodwill is made up of many intangible assets that can’t be readily quantified.

We can all agree that there is value in these assets but the question is, how much? Goodwill is basically the value of the future free cashflow of the business. Based on how your business is structured, it is the value of the profits the business can generate in the future. This is what a buyer is prepared to pay for.

If a buyer has a reasonable certainty of profits and free cashflow in the future, then this is worth something. By comparison, a start-up business will have a higher level of risk and no certainty that profits can be generated. In general, a new business may need to trade for a number of years at a loss before it can establish itself and generate profits. Goodwill is what you are prepared to pay to avoid the risk and the ‘time to establish’ factor.

So, what influences business value and what will people pay for?

- A history of profits, profits, and more profits

- Returns on capital invested (better than 30%)

- Strong growth and growth prospects

- Brand name and value

- A business not dependent on the owners

- A strong, verifiable customer list

- Monopoly income – exclusive territories

- A sustainable competitive advantage

- Good systems and procedures

It is possible to get a price that is widely different from the norm. Unique businesses, unique circumstances, and unique opportunities can always produce ‘an out of the box’ price. If you can build something unique, then you may achieve a price beyond normal expectations. At the end of the day however, the market will set the price.

If you are planning on selling your business, identify who your buyers might be. There could be a purchaser who is prepared to pay a large premium to own your business because of the accretive value or because it is pivotal to their growth strategy.

And, even if you are not thinking about selling your business, the reality is that one day you will. If you build your business with this in mind, then you should look to do the things that will grow your business value from year to year.

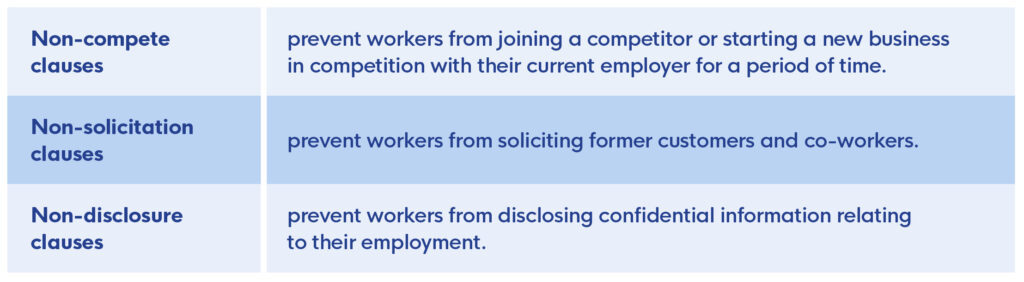

Non-compete clauses and worker restraints under review

A new issues paper from Treasury’s Competition Review questions whether non-competes and other restraints are limiting job opportunities and movement.

A recent Australian Bureau of Statistics (ABS) survey found that 46.9% of businesses surveyed used some kind of restraint clause, including for workers in non-executive roles. The survey also found 20.8% of businesses use non-compete clauses for at least some of their staff and 68.2% for more than three-quarters of their employees.

Over the last 30 years, Australia has seen a decline in job mobility. Australia is not alone in this and other advanced economies have experienced the same issue. While restraint clauses are not the only factor contributing to the decline – an ageing population and a rise in post-pandemic market concentration in some industries has also contributed, it is specifically the role of restraints that is the focus of the Competition Review issues paper (submissions close 31 May 2024).

From an economic perspective, declining job mobility impacts wage growth and innovation as restraints prevent access to skilled workers within the economy. Productivity is a key concern as Australia’s productivity has declined in the last 20 years.

The review states that, “The direct consequence of a non-compete clause is that it hinders competition among businesses: it disincentivises workers from leaving their current job, creating a barrier to the entry of new businesses and the expansion of existing businesses.”

For business however, this is the point – restricting the knowledge developed by a worker during their employment from benefiting a competitor, limiting the likelihood of a ‘mass exodus’ of key workers from the business to a competitor, preventing clients from employing key workers, and protecting the value of the business by preventing employees from walking away with customers that were hard won, at a cost, by the business.

However, the impact of restraints appears to be a psychological deterrent given that most are not contested. Of the 115 matters relating to restraints of trade between 2020 and 2023 dealt with by Legal Aid NSW, only one business commenced proceedings in court against a former worker. And, a further study indicates that where employers seek legal redress in the courts, they are more likely than not to fail.

The international trend is to either ban restraints for workers under a certain income level and time limit restraints for higher paid workers, or to limit the duration of restraints generally but specify a level of compensation to the worker for the restraint period.