08 Dec December 2022 Update

Avoiding the FBT Christmas Grinch!

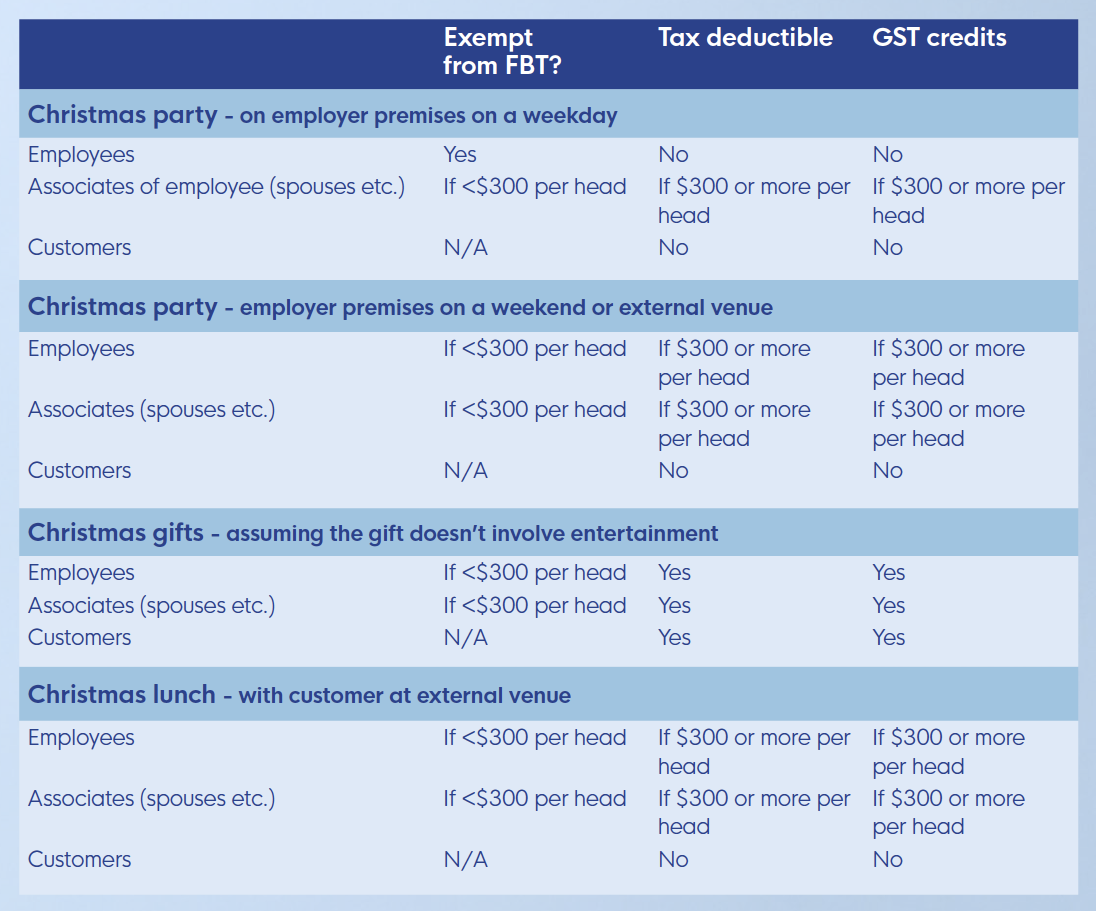

It’s that time of year again – what to do for the Christmas party for the team, customers, gifts of appreciation for your favourite accountant (just kidding), etc. Here are our top tips for a generous and tax effective Christmas season:

Tax & Christmas

For GST registered businesses (not tax exempt) that are not using the 50-50 split method for meal entertainment.

For your business

What to do for customers?

The most effective way of sharing the Christmas joy with customers is not necessarily the most tax effective. If, for example, you take your client out or entertain them in any way, it’s not tax deductible and you can’t claim back the GST. There are specific rules designed to prevent deductions and GST credits from being claimed when the expenses relate to entertainment, regardless of whether there is an expectation of generating goodwill and increased business sales. Restaurants, a show, golf, and corporate race days all fall into the ‘entertainment’ category.

However, if you send your customer a gift, then the gift is tax deductible as long as there is an expectation that the business will benefit (assuming the gift does not amount to entertainment). Even better, why don’t you deliver the gift yourself for your best customers and personally wish them a Merry Christmas. It will have a much bigger impact even if they are not available and the receptionist tells them you delivered the gift

From a marketing perspective, if your budget is tight, it’s better to focus on the customers you believe deliver the most value to your business rather than spending a small amount on every customer regardless of value. If you are going to invest in Christmas gifts, then make it something people remember and appropriate to your business.

You could also make a donation on behalf of your customers (where your business takes the tax deduction) or for your customers (where they receive the tax deduction). Donations to deductible gift recipients (DGRs) above $2 are often tax deductible and can make an active difference to a cause.

What to do for your team?

Christmas is expensive. Some businesses simply can’t afford to do much because cashflow is too tight. Expectations are high so if you are doing something then it’s best not to exacerbate cashflow problems and take advantage of any tax benefits or concessions you can.

Christmas parties

If you really want to avoid tax on your work Christmas party then host it in the office on a workday. This way, Fringe Benefits Tax (FBT) is unlikely to apply regardless of how much you spend per person.

Also, taxi travel that starts or finishes at an employee’s place of work is exempt from FBT. So, if you have a few team members that need to be loaded into a taxi after over indulging in Christmas cheer, the ride home is exempt from FBT.

If your work Christmas party is out of the office, keep the cost of your celebrations below $300 per person if you want to avoid paying FBT. The downside is that the business cannot claim deductions or GST credits for the expenses if there is no FBT payable in relation to the party.

If the party is held somewhere other than your business premises, then the taxi travel is taken to be a separate benefit from the party itself and any Christmas gifts you have provided. In theory, this means that if the cost of each item per person is below $300 then the gift, party and taxi travel can potentially all be FBT-free. Just remember that the minor benefits exemption requires a number of factors to be considered, including the total value of associated benefits provided across the FBT year.

If entertainment is provided to employees and an FBT exemption applies, you will not be able to claim tax deductions or GST credits for the expenses.

If your business hosts slightly more extravagant parties and goes above the $300 per person minor benefit limit, you will pay FBT but you can also claim a tax deduction and GST credits for the cost of the event. Just bear in mind that deductions are only useful to offset against tax. If your business is paying no or limited amounts of tax, a tax deduction is not going to help offset the cost of the party.

Christmas gifts for staff

$300 is the minor benefit threshold for FBT so anything at or above this level will mean that your Christmas generosity will result in a gift to the Tax Office as well at a rate of 47%. To qualify as a minor benefit, gifts also have to be ad hoc – no monthly gym memberships or giving one person multiple gift vouchers amounting to $300 or more.

Gifts of cash from the business are treated as salary and wages – PAYG withholding is triggered and the amount is subject to the superannuation guarantee.

Aside from the tax issues, think about what will be of value to your team. The most appreciated gift is the one that means something to the individual. Giving a bottle of wine to someone who doesn’t drink, chocolates to a health fanatic, or time off to someone with excess leave, isn’t going to garner much in the way of goodwill. A sincere personal message will often have a greater impact than a standard gift.

Missed the director ID deadline? Now what?

If you missed the 30 November 2022 deadline for obtaining a Director ID, the Australian Business Registry Services have stated that they will not take action against directors that apply for their ID by 14 December 2022.

If you are required to but have not yet applied for your ID, you should seek an extension immediately to avoid fines and penalties applying (https://www.abrs.gov.au/sites/default/files/2021-10/Application_for_an_extension_of_time_to_apply_for_a_director_ID.pdf), or contact the ABRS on 13 62 50 (+61 2 6216 3440 outside of Australia).

What do the ‘Secure Jobs, Better Pay’ reforms mean?

The Government’s ‘Secure Jobs, Better Pay’ legislation passed Parliament on

2 December 2022. We explore the issues.

The Fair Work Legislation Amendment (Secure Jobs, Better Pay) Bill 2022 passed Parliament on 2 December 2020. The legislation is extensive and brings into effect a series of changes and obligations that will impact on many workplaces.

The Bill also addresses many of the complexities of the enterprise bargaining process by streamlining the initiation and approval process. For example, to initiate bargaining to replace an existing single-employer agreement, unions and representatives no longer need a majority work determination and instead can make the request to initiate bargaining in writing to the employer.

Fact sheets on key elements of the ‘Secure Jobs, Better Pay’ legislation will be available on the Department of Employment and Workplace Relations website. Please seek advice from a professional industrial relations specialist if your business is impacted.

Fixed term contracts limited to 2 years

Employers are prohibited from entering into fixed-term employment contracts with employees for a period of longer than two years (in total across all contracts). The prohibition also prevents a fixed term contract being extended or renewed more than once for roles that are substantially the same or similar. Some exclusions exist such as for casuals, apprentices or trainees, high income workers ($162k pa), work covering peak periods of demand, where the work is performed by a specialist engaged for a specific and identifiable task, or where the modern award or FWA allows for longer fixed term contracts.

Employers will need to provide employees with a Fixed Term Contract Information Statement (to be drafted by the Fair Work Ombudsman) before or as soon as practicable after entering into a fixed term contract.

From 1 January 2023, the maximum penalty for contravening the 2 year limitation is $82,500 for a body corporate and $16,500 for an individual.

If your workplace has existing fixed term contracts in place, it will be important to review the operation of these to ensure compliance with the new laws.

Gender equality and addressing the pay gap

The concept of gender equality is now included as an object in the Fair Work Act. Previously, to grant an Equal Remuneration Order (ERO) the Fair Work Commission (FWC) assessed claims utilising a comparable male group (male comparator). The legislation removes this requirement opening the way for historical gender based undervaluation to be taken into account and for the FWC to issue a ERO on that basis. That is, female dominated industries may be undervalued generally not specifically compared to men working in that industry or sector. The FWC is no longer required to find that there is gender-based discrimination in order to establish that work has been undervalued. And, the FWC will be able to initiate an ERO on its own volition without a claim being made.

Pay secrecy banned

Prohibits pay secrecy clauses in contracts or other agreements and renders existing clauses invalid.

Employees are not compelled to disclose their remuneration and conditions but have a positive right to do so.

Flexible work requests strengthened

Provides stronger access to flexible working arrangements by enabling employees to seek arbitration before the FWC to contest employer decisions or where the employer has not responded to a request for flexible work conditions within the required 21 days.

If an employer refuses a request for flexible work conditions, the requirements for refusal have been expanded so that employers must discuss requests with the employee and genuinely try and reach agreement prior to refusing an employee’s request. Now, to refuse a request the employer must have:

- Discussed the request with the employee; and

- Genuinely tried to reach an agreement with the employee about making changes to the employee’s working arrangements that would accommodate the employee’s circumstances; and

- the employer and employee have been unable to reach agreement;

- the employer has had regard to the consequences of the refusal for the employee; and

- the refusal is based on reasonable business grounds.

The provisions also expand the circumstances in which an employee may request a flexible working arrangement, for example where they, or a member of their immediate family or household, experiences family or domestic violence.

Accountability for sexual harassment in the workplace

The amendments introduce stronger provisions to prevent sexual harassment and a new dispute resolution framework. Employers may be vicariously liable for acts of their employees or agents unless they can prove they took all reasonable steps to prevent sexual harassment. The amendments build on the Respect@Work report and the Anti-Discrimination and Human Rights Legislation Amendment (Respect at Work) Bill 2022 that passed Parliament in late November 2022. Broadly, the amendments:

- Apply to workers, prospective workers and persons conducting businesses or undertakings; and

- Create a new dispute resolution function for the FWC that enables people who experience sexual harassment in the workplace to initiate civil proceedings if the FWC is unable to resolve the dispute.

Anti-discrimination

Adds special attributes to the FWA to specifically prevent discrimination on the grounds of breastfeeding, gender identity and intersex status.

Aligning pay rates in job advertising with the FWA

Prohibits employers covered by the FWA from advertising jobs at a rate of pay that contravenes the FWA or a fair work instrument. For piecework, any periodic rate of pay to which the pieceworker is entitled needs to be included. The measure addresses concerns raised by the Migrant Workers’ Taskforce and the Senate Unlawful Underpayments Inquiry.

Multi-employer enterprise bargaining

The reforms make it easier for unions/applicants to negotiate pay deals across similar workplaces with common interests creating two new pathways for multi-employer agreements, supported bargaining, and single-interest. The FWC will need to authorise the multi-employer bargaining before it commences.

Supported bargaining for low paid industries

Applies to low-paid industries and is intended to support those who have difficulty negotiating at a single enterprise level – e.g., aged care, disability care, and early childhood education and care. The Minister will have authority to declare an industry or occupation eligible for supported multi-employer bargaining (MEB) and the FWC will decide if it is appropriate for the parties to bargain together. The employer does not have to give their consent to be included.

Employers cannot negotiate a separate agreement once they are included in supported multi-employer bargaining – they need to apply to the FWC to be removed from the supported bargaining authorisation.

Single interest multi-employer bargaining

Single interest multi-employer bargaining draws together employers with “common interests”. These may include geographical location, regulatory regime, and the nature of the enterprise and the terms and conditions of employment. It’s a very broad test.

Unless the employer consents, the FWC will not authorise multi-employer bargaining where it applies to a business with fewer than 20 employees. For businesses with less than 50 employees, to be excluded, the employer needs to prove that they are not a common interest employer or its operations and business activities are not reasonably comparable with the other employers.

For the FWC to authorise single interest multi-employer bargaining, the applicant will need to prove that they have the majority support of the relevant employees.

‘Zombie’ enterprise agreements

A Productivity Commission report found that 56% of employees covered by an enterprise agreement are on an expired agreement, or ‘zombie agreement’. Prior to the reforms, pre 2009 enterprise agreements could operate past their expiry date unless they were replaced with new agreements or terminated by the FWC. As these ‘zombie agreements’ remained fully enforceable, despite being expired, the terms of the agreement were often out of sync with modern awards. The Government notes one zombie agreement terminated in January 2022 saw employees $5 per hour on Saturdays, $10 per hour on Sundays and $24+ per hour on public holidays, worse off than the relevant modern award. The ‘Secure Pay, Better Pay’ reforms generally sunset these zombie agreements.

Important: This article is for information only. If your workplace is likely to be impacted by the amendments, please ensure you seek professional assistance from an industrial relations specialist. We are not specialists and cannot assist with the application of industrial law, awards, or applicable pay rates.