13 Oct October 2022 Update

To cut or not to cut? Stage three personal tax cuts

In September, amid a climate of startling interest rates, UK Chancellor Kwasi Kwarteng announced a series of tax cuts, including the reduction of the top personal income tax rate that applies to those earning more than £150,000 from 45% to 40%. Just ten days later, following market turmoil that saw the British Pound drop at one point to a low of $1.035 USD, its lowest level since 1985, the decision was reversed calling the cuts “a massive distraction.”

Heading into the 2022-23 Federal Budget on 25 October, the question for the Australian Government is different. It is not whether to introduce personal income tax cuts but whether to keep, amend or repeal the cuts legislated to commence on 1 July 2024.

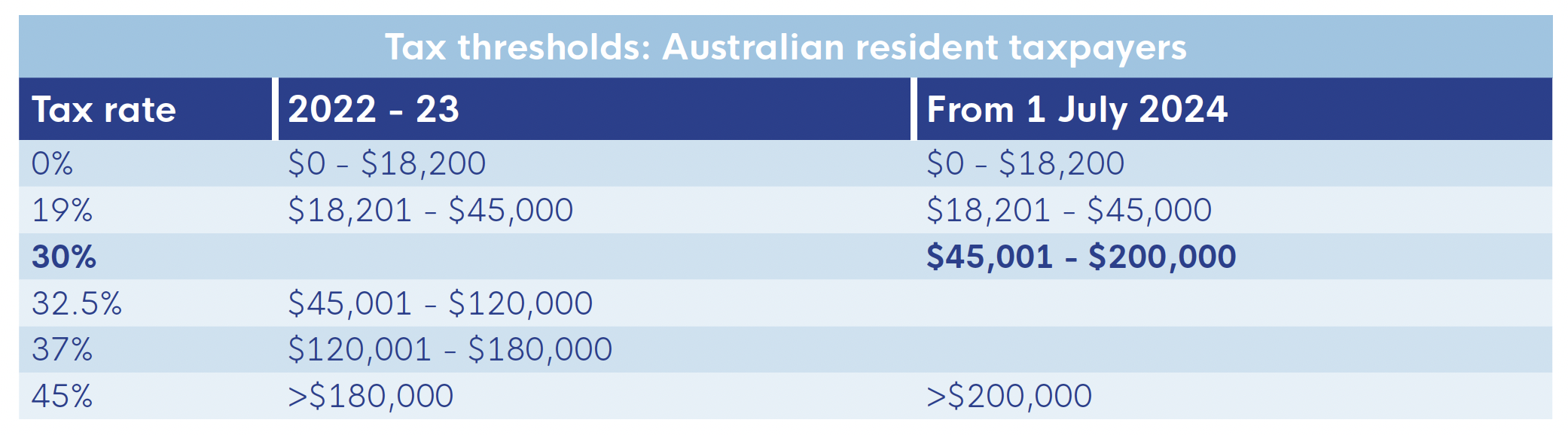

In Australia, the 2018-19 Budget introduced the Personal Income Tax Plan. The plan implemented three stages of income tax cuts over seven years that will, by 2024-25, simplify the tax brackets and enable taxpayers to earn up to $200,000 before paying a new top marginal tax rate of 45%. Stages of the plan, bringing relief for low and middle income earners, were brought forward in the 2019-20 Budget and again in 2020-21.

Labor’s pre-election Lower Taxes policy states, “An Albanese Labor Government will deliver tax relief for more than 9 million Australians through the legislated tax cuts that benefit everyone with incomes above $45,000.” But this month, the Treasurer has subtly changed the narrative from simply “our policy has not changed on stage three tax cuts” to “We do need to ensure that spending in the Budget, particularly in these uncertain global times, is geared toward what’s affordable and sustainable and responsible and sufficiently targeted. I think that’s one of the lessons from the UK.”

The public appeal of repealing the final stage three tax cuts is understandable. Back in 2018-19 when the plan was first introduced, the economy was in surplus and Australia was yet to feel the effects of a global pandemic, environmental extremities, and the Russian invasion of Ukraine. The tax cuts forego around $240bn of tax revenue over the next 10 years, and because it is percentage based, favours high income earners. The public policy think tank, the Grattan Institute, previously warned that if the government progressed with the stage three cuts “Australia’s income tax system will be less progressive than it’s been since the 1950s”.

Conversely, the rationale for reforming the current personal income tax regime where the highest marginal tax rate applies from around 2.5 times average full-time earnings (compared to around 4 times in Canada and 8 times in the US), is also understandable. When it comes to international competitiveness, New Zealand’s top marginal tax rate is 33% (from $180,000) and Singapore’s is 22%, increasing to 24% in 2023-24. If implemented, stage 3 of the income tax plan would see around 95% of taxpayers paying a marginal tax rate of 30% or less.

The 1 July 2024 tax cuts

Stage three of the Personal Income Tax Plan is legislated to take effect from 1 July 2024.

What the tax stats say

Personal income and withholding tax represents around 48% of the annual Commonwealth tax collections. Company tax, by comparison, is around 16%, and the goods and services tax (GST) just under 15% of total tax revenue collected.

Australia has a progressive personal tax system. That is, those with higher incomes pay not only a higher amount of tax, but a higher proportion of their income in tax. As a result, the 3.6% of taxpayers with taxable incomes of over $180,000 pay 31.6% of the total.

Where to from here?

The second 2022-23 Federal Budget will be announced on 25 October 2022. If the Government make no mention of the stage three tax cuts, they have another opportunity to refine their position in the 2023-24 Federal Budget released in May 2023, more than a year before the 1 July 2024 tax cuts come into effect.

Our best guess? The Government will announce a review of the stage three tax cuts, then open the issue to consultation, locking in the position, whatever it is, in the 2023-24 Federal Budget.

We’ll keep you posted!

Look out for our 2022-23 Federal Budget update on 26 October!

States move on property based taxes

Queensland backs down on Australia wide land tax assessment

The Queensland Government has backed away from an amendment that would have seen the land tax rate for investment property in Queensland assessed on the value of the investor’s Australia wide land holdings from 1 July 2023, not just the value of their Queensland property.

The amendment passed the Queensland Parliament and became law on 30 June 2022. The amendment would see the value of all of the landholder’s Australian investment property assessed, the value of Queensland land tax calculated on taxable Australian wide investments, then apportioned to the Queensland portion of the land. The amendment requires the landholder to declare their interstate landholdings and data from other sources to verify the landholdings. The end result is many investors being tipped into a higher land tax rate.

The Bill states, “The land tax reform is intended to make Queensland’s land tax system fairer by addressing an inequity which can result in a landholder with all of their landholdings in Queensland paying more land tax than a landholder with a similar value of landholdings spread across jurisdictions.”

Following the National Cabinet Meeting on 30 September, Premier Palaszczuk rescinded the reform as it relied on the “goodwill of other states, and if we can’t get that additional information, I will put that aside.”

Stamp duty or an annual property tax for NSW first home buyers?

First home buyers purchasing property in NSW of up to $1.5m will have a choice of paying stamp duty or an annual property tax from 16 January 2023.

The annual property tax payments will be based on the land value of the purchased property. The property tax rates for 2022-23 are:

- $400 plus 0.3% of land value for properties whose owners live in them

- $1,500 plus 1.1% of land value for investment properties.

Property tax assessments will be issued annually to home buyers who take the annual property tax option. As an example, a first buyer purchasing a $1.2m NSW property with a land tax value of $720,000, could pay stamp duty of $50,875 or opt to pay the annual property tax ($2,560 for 2022-23). The property tax rates will be indexed annually.

Eligible first home buyers who sign a contract of purchase on or after 16 January 2023 will be eligible to opt into the property tax. If the property tax option is selected, first home buyers must move into the property within 12 months of purchase and live in it continuously for at least 6 months.

The annual property tax is only applicable to the purchaser. If the property is sold, the property tax does not apply to subsequent purchasers. For eligibility details, see First Home Buyer Choice on the NSW Government website.

Legislation enabling the property tax is expected before the NSW Parliament this month. If passed, eligible first home buyers who sign a contract of purchase between the passage of the legislation and 15 January 2023 will be eligible to opt into the property tax. These purchasers will pay land stamp duty but will be able to apply for and receive a refund of that duty if they opt into property tax.

COVID downgraded but not gone

National Cabinet agreed to end the mandatory isolation requirements for COVID-19 effective from 14 October 2022. Each state and territory has, or will, implement the end of the isolation rules.

The Pandemic Leave Disaster Payment, the payment to workers who have lost income they needed to self isolate or care for someone with COVID-19, also end on 14 October. The Pandemic Leave Disaster Payment was extended beyond its 30 June end date but restricting the number of times claims can be made in a 6 month period.

While the Pandemic Leave Disaster Payment will end, National Cabinet agreed to continue targeted financial support for casual workers, on the same basis as the disaster payment, for workers in aged care, disability care, aboriginal healthcare and hospital care sectors. Final details of this new payment are yet to be released.

ATO contacts ‘at risk’ professional services firms

New guidelines for professional services firms – lawyers, architects, medical practitioners etc., came into effect on 1 July 2022. The guidance takes a strong stance on structures designed to divert income in a way that results in principal practitioners receiving relatively small amounts of income personally for their work and reducing their taxable income. The ATO is now contacting professionals who they believe might be at risk. Any structural changes that need to be made to reduce risk, should be completed by the end of the 2022-23 financial year. Where the ATO deems that income has been diverted inappropriately to create a tax benefit, they will remove that benefit and significant penalties may apply

1 October minimum wage increase

Minimum wages in 10 awards in the aviation, tourism and hospitality sectors increased from 1 October 2022. The increase happens from the first full pay period on or after 1 October 2022. See the Fair Work Ombudsman for more details.

Director ID number deadline looming

If you are a Director of a company or registered foreign company and have not applied for your Director ID Number, the deadline is 30 November 2022. Don’t leave it until the last minute!

Australian super funds gorge on cryptocurrency

The value of cryptocurrency assets inside Australian self managed superannuation funds (SMSFs) increased by 589.9% ($1.17bn) between June 2019 and June 2022, according to the latest ATO statistics.

While cryptocurrency is a relatively small asset class at only 0.16% of the $837bn held in SMSFs, it is a growing asset class, larger than collectibles and personal use assets, and overseas property.

Smaller funds, with an asset value below $200,000, are more likely to have a larger proportion of their value in cryptocurrency.

ASIC warns of SMSF cryptocurrency scams

Earlier this year, the Australian Securities and Investments Commission (ASIC) issued a warning on an increase in marketing encouraging Australians to switch from retail superannuation funds to SMSFs so they can invest in ‘high return’ portfolios. The regulator states that crypto-assets are a high risk and speculative investment and best practice is to seek advice from a licensed financial adviser before agreeing to transfer superannuation out of a regulated fund into an SMSF.

An example of one of these schemes was A One Multi Services Pty Ltd that was shut down by ASIC late last year. The company promoted a scheme encouraging investors to roll their superannuation into an SMSF, then for the SMSF to loan money to A One Multi to generate “returns of between 10% and 20% on the investment and perhaps as high as 26%.” Over 60 SMSFs transferred $25 million into A One Multi’s accounts between January 2019 and June 2021. The money “invested” for the clients, between $7 million to $22 million of Bitcoin, was held in the name of one of the directors. An additional $5.7m was used by the directors to acquire property and luxury cars.

Investing in crypto

Trustees are free to invest in assets that meet the requirements of the fund and comply with the regulatory requirements:

- Trust Deed – must allow for cryptocurrency assets. Most SMSF trust deeds are drafted broadly to enable trustees to invest in assets permitted by the superannuation laws and leave the investment strategy to manage the choice of assets and their appropriateness. However, it is important to check.

Investment strategy – With cryptocurrency’s high volatility and risks, there must be clearly articulated information in the Investment Strategy. That is, it must articulate the trustees’ plan for making, holding and realising assets in a in a way that is consistent with the retirement goals of members being mindful of the member’s individual circumstances.

- Separation of assets – cryptocurrency assets must be held in a wallet in the name of the SMSF and the IP address is provided to the SMSF auditors to verify the transactions (against the fund bank account). Problems often arise when a wallet (in the name of the SMSF) is connected to a personal credit card to acquire cryptocurrency. In these cases, the payment may be considered as either a contribution or a loan to the SMSF.

- Sole purpose test – Your SMSF needs to meet the sole purpose test to be eligible for the tax concessions normally available to super funds. This means your fund needs to be maintained for the sole purpose of providing retirement benefits to your members, or to their dependants if a member dies before retirement.

Lessons from a data breach

The Optus data breach is top of mind for a lot of Australians, particularly those who have had their data breached.

For business, the breach is a timely warning on the importance of understanding what data is held on your customers (and should you hold it?), how it is secured, how your systems work and the process to identify gaps and deficiencies, the appropriate actions if and when a breach occurs, and the impact on your relationship to your customer. This is not something that can be outsourced to IT but a whole of business issue.

The obligations on business

We all know that no system is 100% secure. For Optus, this is not the first time. In 2015, Optus agreed to an enforceable undertaking for breaching the Privacy Act in 2015.

A data breach happens when personal information is accessed or disclosed without authorisation or is lost. If the Privacy Act 1988 covers your business, you must notify affected individuals and the Office of the Australian Information Commissioner when a data breach involving personal information is likely to result in serious harm. The notification must be as soon as practicable but is expected to be no later than 30 days. Every day counts.

A business must take all reasonable steps to comply with its obligations to prevent data breaches occurring. These obligations are not limited to preventing cyber attacks. Malicious or criminal attacks represent 55% of all reported data breaches. But, human error is responsible for 41% and 4% through system faults. Where human error was involved, 43% was where personal information was emailed to the wrong recipient and 21% the unintended release or publication of personal information.

How to apologise

Your relationship with your client is about trust. Beyond the breach notification requirements, the other issue is the client relationship.

So, how should a business apologise? University of Chicago economist John List, Professor Benjamin Ho from Vassar College along with other academics studied this issue for Uber ride sharing – the experiment came about after John List, who was at the time Uber’s Chief Economist, had a bad ride sharing experience. The bottom line? The apology must come at a cost to be effective. That cost can be reputational, a commitment to do better in the future (the cost is the higher standard), or a monetary cost. The paper states: First, apologies are not a panacea – the efficacy of an apology and whether it may backfire depend on how the apology is made. Second, across treatments, money speaks louder than words – the best form of apology is to include a coupon for a future trip. Third, in some cases sending an apology is worse than sending nothing at all, particularly for repeated apologies and apologies that promise to do better.

Helping to protect against data breaches

- Understand your Privacy Act obligations. Specific industries and businesses that hold specific types of data often have advanced requirements.

- Review the personal information held on customers. Is their full date of birth a necessary part of what your business does? If you need to verify identify, do those identification documents really need to be stored once they have been validated? Or is positive confirmation enough? Is the data held securely and is access limited to only those who require access?

- Ensuring systems have multifactor authentication

- Improving staff awareness of not only cyber threats and how to prevent them – phishing, fraudulent messages etc, but reviewing how personal data is managed and accessed.

- Understanding your systems and how they work together to prevent security gaps or ‘backdoor’ systems access.